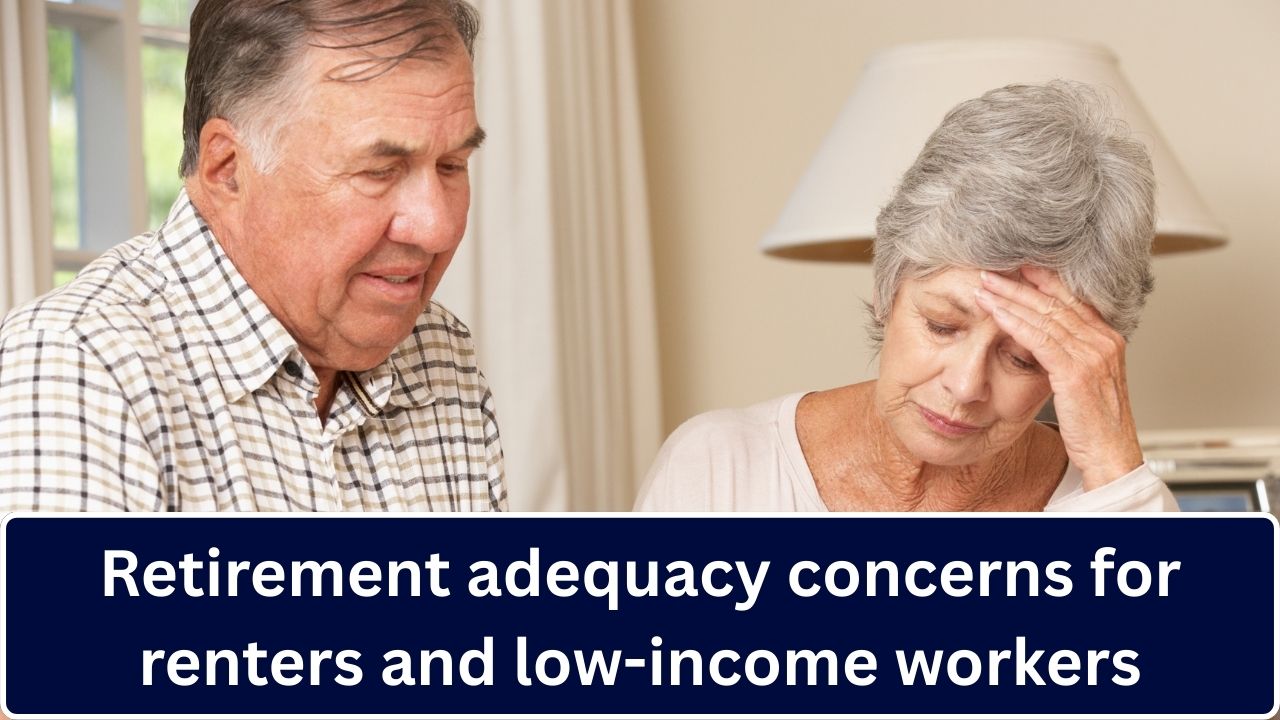

As dawn breaks in a small apartment complex outside Manchester, 62-year-old Elaine Turner locks her front door and watches neighbors leave for early shifts. With no savings and a lifetime of renting, she wonders if retirement will ever arrive as financial security rather than continuing worry.

Across the UK, US, Australia, New Zealand, and Canada, millions of renters and low-income workers are confronting a stark reality: existing retirement systems were never designed for their financial profiles. With rising housing costs, weak pension coverage, and insecure employment, older workers face the very real prospect of spending their later years in poverty.

“Rent eats everything,” says Elaine. “By the time I pay bills, there’s nothing left for a pension. I feel like I’m always behind.”

Here’s what you need to know about this growing challenge.

What’s New: Mounting Pressures on Retirement Security

• Housing costs outpacing savings — Across major cities from London to Toronto, rent increases have far outpaced wage growth and pension contributions.

• Coverage gaps in pension systems — Millions in casual, gig, or part-time work lack access to employer retirement plans.

• Low-income workers disproportionately affected — Even with long employment histories, limited earnings translate to negligible retirement savings.

• Policy responses lag need — Governments are exploring reforms, but change is slow compared to the urgency on the ground.

Real Stories Behind the Policy

In the US, 58-year-old Joe Ramirez has worked in warehouses for decades, often moving between shifts and employers. “I thought Social Security would take care of me,” he says. “But my earnings were low and intermittent — what I’m projected to get is barely above poverty.”

In Auckland, New Zealand, lifelong renter Tania Ngatai had intended to save through KiwiSaver, but rent hikes consumed her income. “Every time I tried to put more away, rent jumped again,” she says. “Now I’m not sure I’ll ever retire.”

These are not isolated stories. Data show systemic shortcomings that leave low-income households ill-equipped for retirement.

Government Statements

In recent parliamentary sessions, officials have acknowledged the issue:

- UK Department for Work and Pensions spokesperson: “We recognize that housing affordability and low pension participation among workers with irregular employment patterns require targeted policy responses.”

- US Social Security Administration: “Ensuring retirement adequacy is central to our mission. We are evaluating proposals to strengthen benefits for low-income retirees.”

- Australian Treasury: “We remain committed to examining superannuation mechanisms to better support low-income and vulnerable workers.”

- New Zealand Minister of Seniors: “Retirement income policy must keep pace with changes in work and housing markets.”

- Canadian Minister of Seniors: “We are exploring enhancements to Old Age Security and Guaranteed Income Supplement to address rising cost pressures.”

Expert Analysis / Data Insight

Housing Costs vs. Savings: In many major urban centers, average rent now exceeds 30–40% of income for low-income households — a level that leaves little room for savings or retirement contributions.

Pension Coverage Gaps:

- In the US, nearly 1 in 3 private-sector workers lacks access to employer-sponsored retirement plans.

- In the UK and Canada, self-employed and gig workers remain underrepresented in pension systems.

- Australia’s superannuation reaches many workers, but casual and part-time employees still miss out on contributions.

Projected Retirement Incomes: Analysts forecast that without reform, a growing share of retirees will rely heavily on state benefits, with limited supplemental savings to maintain living standards.

Comparison Table: System Features and Gaps

| Country | Pension System | Coverage Challenges | Housing Cost Pressure | Policy Moves Underway |

|---|---|---|---|---|

| UK | State Pension + auto-enrolment | Low coverage for self-employed | High in London & South | Exploring minimum contribution increases |

| US | Social Security + employer plans | Gig & part-time gaps | Severe in major metros | State-level savings programs expanding |

| Australia | Mandatory Superannuation | Casual workers miss contributions | Rising in Sydney/Melbourne | Proposed low-income credit boosts |

| New Zealand | NZ Super + KiwiSaver | Renters struggle to save | High in Auckland | KiwiSaver contribution incentives |

| Canada | CPP/QPP + employer plans | Coverage uneven | High in Vancouver/Toronto | CPP enhancement discussions |

Why Renters and Low-Income Workers Are at Risk

1. Limited Retirement Contributions

Many retirement systems tie savings to formal employment. Renters and low-income workers are:

- More likely to have irregular hours

- Employed in small firms without retirement plans

- Part of the gig economy without automatic contributions

2. Housing Costs Erode Savings Potential

When rent consumes the bulk of income, there’s little left for pension contributions, emergency buffers, or investment accounts.

3. Longer Life Expectancy Raises Risk

As people live longer, retirement periods lengthen — requiring more savings. Without adequate funds, retirees risk outliving their resources.

What You Should Know

For Renters

- Explore local pension schemes or government savings options.

- Prioritize even small contributions — consistency builds security.

- Understand rental assistance and housing benefit programs to free up income for savings.

For Low-Income Workers

- Seek out employer plans when available; if not, consider individual retirement accounts where possible.

- Take advantage of government incentives (e.g., matching contributions).

- Track projected retirement income using official tools (e.g., My Social Security in US, Pension Wise in UK).

For Retirees Nearing Retirement

- Review benefit eligibility early.

- Consider phased retirement options.

- Seek financial counseling offered by government or not-for-profit organizations.

Q&A: Clarifying Common Concerns

1. Why do renters struggle more with retirement savings?

Renters often face high housing costs that leave minimal disposable income for retirement contributions.

2. Can government pensions alone support retirees?

In many countries, state pensions provide a base level of income but may not sustain living standards without additional savings.

3. Do low-income workers have any special retirement benefits?

Some countries offer credits or supplemental benefits for low earners — check your local programs.

4. What about gig economy workers?

They often lack employer contributions, making personal savings plans essential.

5. Are automatic enrollment programs helping?

Yes, auto-enrolment increases participation but may not fully address adequacy without sufficient contribution levels.

6. How does rising rent affect future retirees?

Higher rent reduces ability to save and can delay retirement.

7. Are there tax incentives for retirement savings?

Many nations offer tax advantages to encourage saving — understanding them can boost your retirement funds.

8. What if I’m already close to retirement with little saved?

Explore delayed retirement credits and maximize state benefits; seek free financial counseling.

9. Can policy changes help future generations?

Yes — proposals include expanding coverage, increasing contributions, and enhancing safety nets.

10. How can employers help?

By offering inclusive plans and facilitating contributions for part-time and casual staff.

11. What is “adequate” retirement savings?

A rule of thumb is replacing 60–80% of pre-retirement income, though individual needs vary.

12. How Do Housing Markets Tie into Retirement Policy?

Affordable housing policies can free up income for savings and improve retirement outlooks.

13. Should renters buy property to secure retirement?

Homeownership isn’t feasible for all; secure tenure and savings stability matter more than ownership alone.

14. Do changes in life expectancy affect retirement planning?

Longer lives mean needing more savings — planning sooner is better.

15. What’s the first step for someone concerned about retirement?”

Get a clear picture of your projected income and benefits and seek tailored planning advice.

Leave a Comment